- Case Study published on 09 Jun 2026

- - Superannuation

Question:

I am 55 years old and have never made a tax deductible superannuation contribution in the past. I earn $110,000 and have roughly $550,000 in Super benefits. Is it worthwhile my making a top up tax deductible super contribution?

The short answer:

Yes — for someone in this position, a tax-deductible contribution is usually worth a serious look. The main reason is simple: money you put into super as a concessional (before-tax) contribution is taxed at 15%, while the same money taken as salary is taxed at your marginal rate, which at this income is 32% including the Medicare levy. That gap is where the saving comes from.

Why it works:

A tax-deductible super contribution is just money you add to your retirement savings before tax is applied. Instead of that money being taxed as ordinary income, it is taxed at the lower rate that applies inside super. For most people earning a salary like this, that means paying less tax now while putting more away for later.

At 55, this is often the point where people start checking how prepared they are for retirement, and where relatively small adjustments can add up over the years that remain. A balance of around $550,000 is a solid foundation, and topping it up in a tax-effective way can strengthen it further.

Things to keep in mind:

- There is a yearly limit. You can only contribute a set amount each year . For 2025–26 that cap is $30,000, and it includes the super your employer pays. Going over the cap can trigger extra tax, which eats into the benefit.

- Your money is locked away. Contributions are generally preserved until you meet a condition of release in retirement. At 55, that can mean several years before you can access the funds. This enforces good savings discipline, but it reduces flexibility if you need the money sooner.

- Your wider position matters. If you have manageable expenses, little debt, and some accessible savings outside super, extra contributions can be an effective way to boost retirement income while cutting tax. If you expect large expenses soon or prefer easy access to cash, a more gradual approach may suit you better.

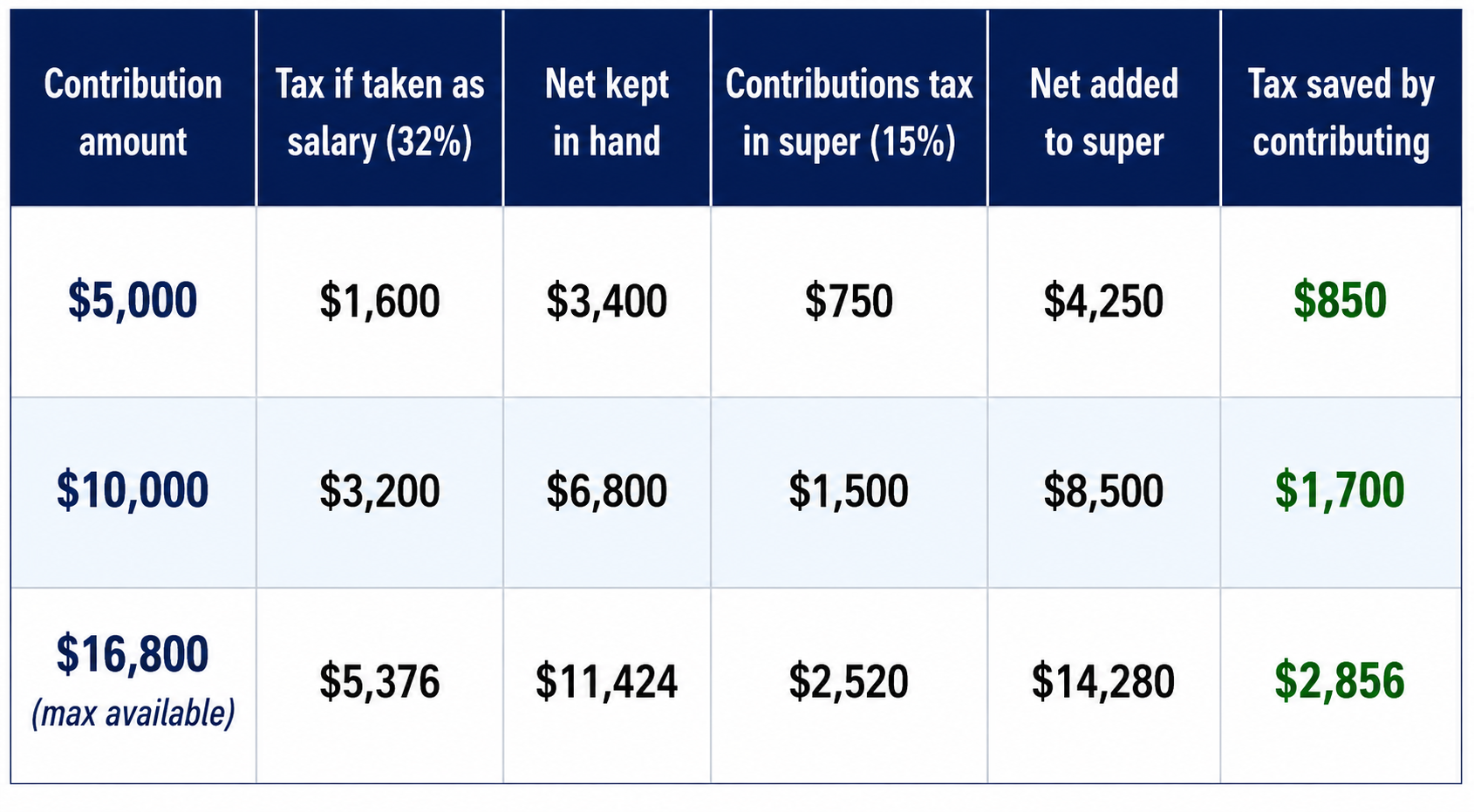

A side-by-side example:

The clearest way to see the benefit is to compare the two choices directly: take the money as ordinary salary, or direct it into super as a tax-deductible contribution. The table below illustrates this for the example above — a 55-year-old earning $110,000 with around $550,000 already in super — using 2025–26 tax rates and contribution caps.

The figure to focus on is the difference in tax treatment. Income at this level is taxed at 32% (including the Medicare levy), while a concessional contribution is taxed at just 15% inside super. That 17-cents-in-the-dollar gap is the source of the saving shown in the final column.

These figures are illustrative only. The example relies on specific assumptions — how much employer super has already been paid, the available cap, eligibility for catch-up contributions, and the individual's cash flow and goals. Your own position may differ in any of these respects, and even small differences can change the outcome. The numbers are intended to show the principle, not to recommend a particular course of action. Every individual's circumstances require specific, tailored advice before acting.

Assumptions used in the example:

- 2025–26 financial year, salary of $110,000 (super guarantee paid on top).

- Marginal tax rate on this income: 30% + 2% Medicare levy = 32%.

- Tax on concessional contributions inside super: 15%.

- Concessional (before-tax) cap: $30,000. Employer super guarantee of $13,200 (12% × $110,000) already counts toward it, leaving roughly $16,800 of room for a personal deductible contribution.

- Not eligible for "carry-forward" catch-up contributions, because that requires a total super balance under $500,000 at the prior 30 June (this person has ~$550,000).

Take it as salary vs. contribute it to super:

Based on the maximum available contribution of $16,800, you will save around $2,856 this year, with $14,280 going into super compared with $11,424 kept in hand. Note that this is the tax saving only — it is separate from any investment growth the money then earns inside the fund.

In summary:

For someone earning $110,000 at age 55 with a healthy super balance, making additional tax-deductible contributions can be a worthwhile way to reduce tax now and build retirement savings — provided the locked-away nature of super and your broader cash flow suit it. Because the right contribution level depends entirely on your personal circumstances, a tailored review through Your Lifetime can help you work out the approach that fits your goals and cash flow.

Why not take the next step and talk to a qualified and highly experienced financial planner today?

LifeTime Financial Group are specialist (holding appropriate accreditations) financial planners who are ideally positioned to work with you in planning and managing your retirement planning needs

If you would like to discuss your current position or wider financial planning needs, why not call us today on 03 9596-7733? There is no cost or obligation for our initial conversation/meeting.

LifeTime Financial Group. A leading privately owned Melbourne-based Financial Planning practice with no ties to any financial institution.

This article provides general information only and does not take your personal objectives, financial situation, or needs into account. It is not personal financial advice. Tax rates, caps, and rules are current as at the 2025–26 financial year and may change. You should seek advice tailored to your own circumstances before acting.