- Published on 07 Jul 2026

- - Superannuation

Unlock the Super You Never Used

How the carry-forward rules turn unused super caps into a real tax break

The tax break hiding in your super statement

Most people assume the $30,000 annual limit on before-tax (concessional) super contributions is strictly use-it-or-lose-it. It isn’t. If you didn’t use your full cap in recent years, the leftover amount doesn’t simply vanish — you may be able to “carry it forward” and use it in a later year. For many Australians, that is a sizeable and often overlooked way to cut a tax bill.

First hurdle: the $500,000 test

There is one gate you must pass. Your total superannuation balance — the combined value of all your super accounts — must have been below $500,000 on 30 June of the previous financial year. For 2025–26, that means your balance at 30 June 2025. Clear that hurdle and you can tap unused cap amounts from the past five financial years.

How the five-year window works

Unused amounts only stretch back five years, and the oldest year drops off first. An unused amount from 2020–21 that you don’t use by the end of 2025–26 expires for good. In practice, someone who contributed little for five years could have a concessional cap as high as $167,500 this year — the $30,000 current cap plus up to $137,500 of catch-up room. The annual cap also rises to $32,500 from 1 July 2026 (the 2026–27 year), so the room available in future years grows too. You don’t need to complete any forms to track this; myGov displays your available amount.

A real example — Priya’s property sale

Priya, 54, returned to part-time work after several years caring for family, so her employer contributions were modest. Her total super balance at 30 June 2025 was $380,000 — under the $500,000 threshold — and myGov shows $82,500 of unused cap across the previous five years. That lifts her concessional cap for 2025–26 to $112,500 ($30,000 plus $82,500).

In 2025–26 Priya sells an investment property, triggering a capital gain and freeing up cash. Her employer will pay about $14,000 in compulsory super this year, leaving $98,500 of room. She contributes $98,500 into super and lodges a Notice of Intent so she can claim it as a tax deduction. That deduction reduces the income she pays tax on — including the capital gain.

Here is where the tax appeal lies. Money you earn is normally taxed at your marginal rate — the rate on your top dollar of income — which climbs as you earn more and can reach 47% once the Medicare levy is included. A concessional contribution is taxed at just 15% on the way into super instead. The wider the gap between those two rates, the more tax you keep in your own pocket, and in a big-income year like Priya’s that gap is at its largest.

Watch these traps

The strategy is powerful, but the detail matters.

- Money you put into super is generally locked away until you reach preservation age (currently 60) and meet a condition of release, so only contribute what you won’t need sooner. You must lodge the Notice of Intent before you claim the deduction.

- Higher earners — broadly those above $250,000 once the contribution is counted — may pay an extra 15% Division 293 tax, though it is usually still worthwhile.

- Moving from Super to Pension — Remember to lodge the Notice of Intent prior to moving your account from Accumulation to Pension phase. Once the funds leave Accumulation phase, the Super administrators cannot recover the 15% (Or 30% - See Div 293 note above) tax on that contribution. And it cannot be undone.

Is it worth it for you?

Carry-forward suits people with lumpy incomes: a bonus year, the sale of an asset, an inheritance freeing up cash, or a return to higher earnings after time out of the workforce. The best first step is to check your unused cap and total super balance in myGov, then confirm the numbers stack up for your own situation before you act.

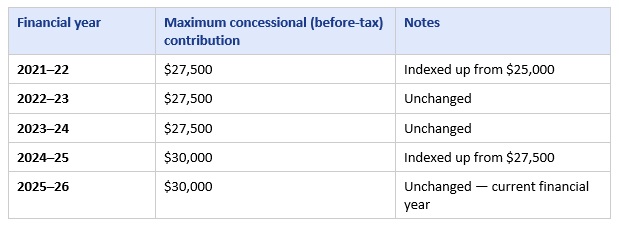

Maximum concessional contribution caps: 2021–22 to 2025–26

The concessional (before-tax) contribution cap is the most you can put into super at the concessional 15% tax rate in a year. It is indexed to wages growth (AWOTE) and rises in $2,500 steps.

These are the standard annual caps only. The amount you can actually carry forward depends on what you contributed each year and on having a total super balance below $500,000 at 30 June of the previous year. The cap rises again to $32,500 from 1 July 2026 (the 2026–27 year).

Why not take the next step and talk to a qualified and highly experienced financial planner today?

LifeTime Financial Group are specialist (holding appropriate accreditations) financial planners who are ideally positioned to work with you in planning and managing your financial planning needs including maxmising your Super carry forward benefits.

If you would like to discuss your current position or wider financial planning needs, why not call us today on 03 9596-7733? There is no cost or obligation for our initial conversation/meeting.

LifeTime Financial Group. A leading privately owned Melbourne-based Financial Planning practice with no ties to any financial institution.

This article provides general information only and does not take your personal objectives, financial situation, or needs into account. It is not personal financial advice. Tax rates, caps, and rules are current as at the 2025–26 financial year and may change. You should seek advice tailored to your own circumstances before acting.

References

- Australian Taxation Office — Concessional contributions cap — https://www.ato.gov.au/individuals-and-families/super-for-individuals-and-families/super/growing-and-keeping-track-of-your-super/caps-limits-and-tax-on-super-contributions/concessional-contributions-cap

- Australian Taxation Office — Contributions caps (key super rates & thresholds) — https://www.ato.gov.au/tax-rates-and-codes/key-superannuation-rates-and-thresholds/contributions-caps

- Australian Taxation Office — Tax rates (Australian residents) — https://www.ato.gov.au/tax-rates-and-codes/tax-rates-australian-residents

-

Australian Taxation Office — Contributions caps (key super rates & thresholds): ato.gov.au/tax-rates-and-codes/key-superannuation-rates-and-thresholds/contributions-caps