- Case Study published on 09 Jun 2026

- - Superannuation

Could a $1,000 Super Top-Up Earn You a Free $500?

If you are working part time and earning around $40,000 a year, you might think extra super contributions are something only higher earners benefit from. The good news is the opposite is often true. Lower income earners have access to one of the most generous boosts in the system.

It is called the government super co-contribution, and it is designed to reward people who add a little of their own money to their retirement savings. For someone in your position, putting in $1,000 of your own after-tax money could see the government add a further $500. That is an immediate 50% boost before your savings have earned a cent.

How it works:

The idea is simple. When you make a personal contribution from money you have already paid tax on, and you earn under a certain amount, the government chips in too. You do not claim a tax deduction for this type of contribution, which is what makes it eligible.

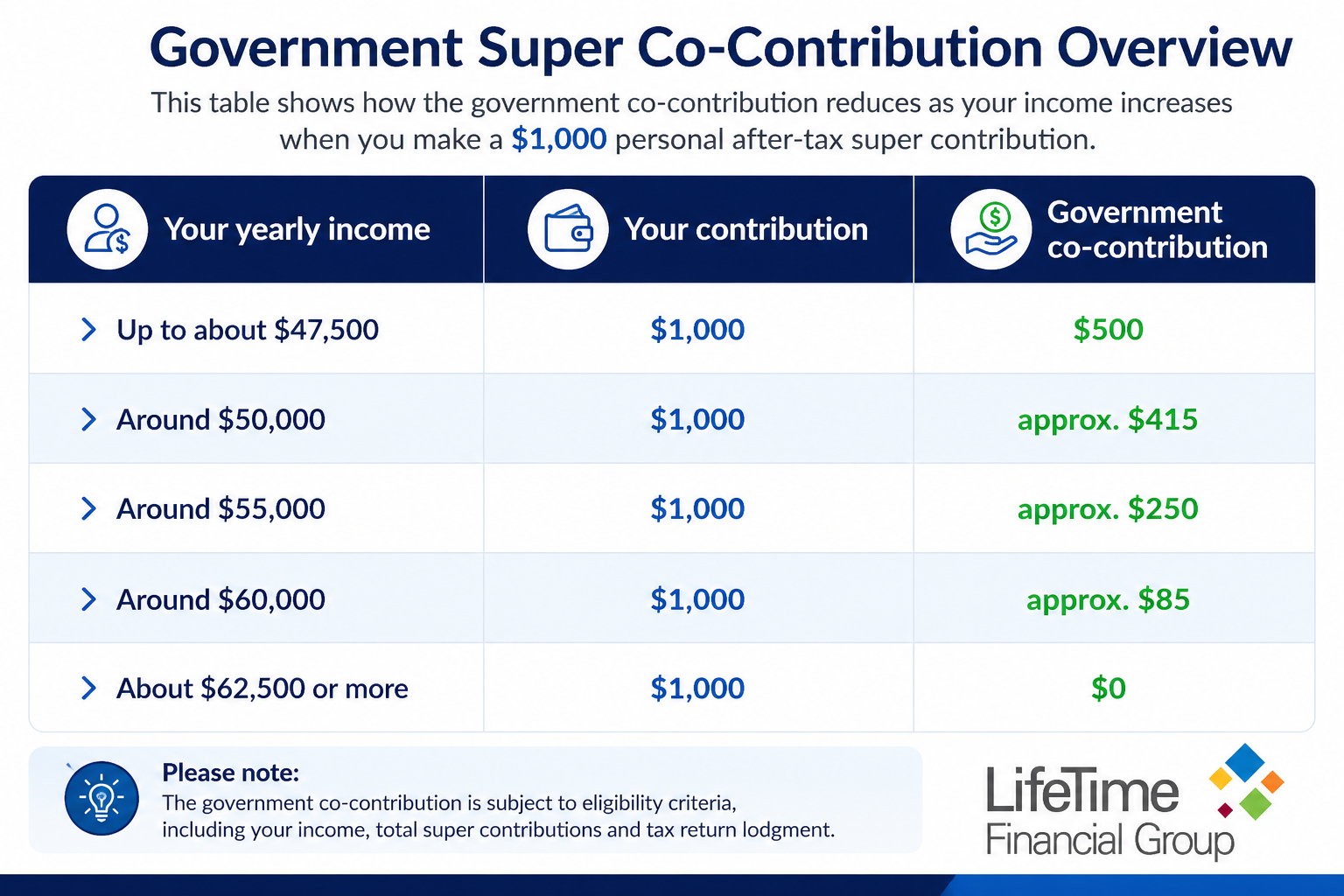

The top-up is 50 cents for every dollar you contribute, up to a maximum of $500. So a $1,000 contribution at your income level attracts the full amount. The benefit gradually reduces as income rises and phases out completely above the upper limit.

What you could receive:

The table below shows how the co-contribution changes with income, assuming you contribute the full $1,000. The exact thresholds are updated each year, so always check the current figures on the HESTA page linked at the end before you act.

Please note table relates to the 2025 - 2026 financial year.

At an income of around $40,000, you sit comfortably under the lower threshold. That means your $1,000 contribution should attract the full $500 top-up, turning your savings into $1,500 straight away.

A few things to check

- There are some simple conditions. You need to lodge a tax return, be under 71 at the end of the financial year, and earn at least part of your income from work or a business. You also need to stay within your contribution limits, which is not a concern at this level.

- The money is locked away until retirement, so only contribute what you can comfortably set aside. For most lower income earners, though, a free 50% return is very hard to beat.

Why not take the next step and talk to a qualified and highly experienced financial planner today?

LifeTime Financial Group are specialist (holding appropriate accreditations) financial planners who are ideally positioned to work with you in planning and managing your retirement planning needs

If you would like to discuss your current position or wider financial planning needs, why not call us today on 03 9596-7733? There is no cost or obligation for our initial conversation/meeting.

LifeTime Financial Group. A leading privately owned Melbourne-based Financial Planning practice with no ties to any financial institution.

This article provides general information only and does not take your personal objectives, financial situation, or needs into account. It is not personal financial advice. Tax rates, caps, and rules are current as at the 2025–26 financial year and may change. You should seek advice tailored to your own circumstances before acting.