- Published on 07 Jul 2026

- - What is Financial Planning?

What Is a Reasonable Fee for a Financial Advisor?

If you have ever asked “what’s a fair price for financial advice?”, you are asking the right question — but only half of it. In Australia, ongoing advice fees commonly sit around 1% p.a. (plus GST), and can run up to about 1.5% p.a. (plus GST) depending on who you use and how complex your affairs are. On a $1 million portfolio, that is roughly $10,000 to $15,000 a year. The number matters — but it is not the whole story.

The advice fee is only one layer

The fee you pay your adviser is separate from the cost of the products and investments your money actually sits in. Two clients can pay an identical advice fee and still end up with very different total costs, purely because of how their money is invested. That second layer — the investment “engine” — is where a lot of cost quietly lives, and it is the part most people never think to ask about.

What LifeTime Financial Group charges

LifeTime Financial Group specailises in more complex client requirements including Family Trusts, self-managed superannuation fund arrangements and Directly Held Investment Portfolios. Our costings reflect that commitment to detail, our deep understanding, our personal relationship with you and your family and, more than 40 years of experience. Our ongoing advice fee (Value client offering) is $4,000 per year (indexed) plus 0.60% of the funds we manage for you. On a $1 million portfolio that works out to $10,000 a year — around 1.0%, at the lower end of the typical Australian range. We think that is fair for genuinely personal, ongoing advice. But we would rather you judged us on the total cost, not just the headline percentage. As funds under management increase , our costs reduce as a percentage of the funds we manage and take responsbility for.

Why the investment method matters just as much

Most large, institutionally-owned platforms invest clients into a portfolio of managed funds, often blended with cash. Each managed fund charges its own annual management cost, and the platform charges an administration fee on top of that. For a diversified portfolio built for a 70% growth risk profile, those managed-fund costs typically add up to roughly 0.80%–1.00% p.a. — before you count a single dollar of advice fee.

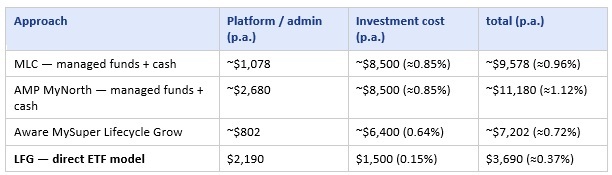

A real-world comparison — $1,000,000, 70% growth

The table below compares the cost of the investment engine only — platform plus investments, before any personal advice fee — across three institutionally-owned approaches and our own direct exchange-traded fund (ETF) model. Figures are illustrative, drawn from each provider’s current published fees; your actual cost depends on the specific funds selected.

Illustrative only. MLC and AMP figures assume a diversified managed-fund portfolio plus cash; managed-fund investment cost is a representative ~0.85% p.a. Aware Super’s MySuper Lifecycle Grow is a low-cost default option — note it actually sits above a 70% growth weighting (81–95% growth).

Confirm all figures against current PDS / fee documents before relying on them.

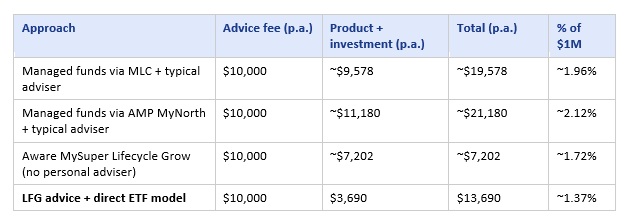

Now add the advice — the all-in picture

A fee comparison only makes sense like-for-like. The next table adds a typical 1.0% p.a. advice fee to the managed-fund options, so every column reflects an advised solution, and sets them against our advice-plus-ETF model. Aware’s MySuper option is shown as-is, because it does not include a personal adviser.

Illustrative only, on a $1,000,000 balance. “Product + investment” repeats the engine cost from the previous table. A typical adviser fee of 1.0% p.a. has been assumed for the MLC, AMP and Aware (Assuming your adviser is approved and engaged by you to manage an Aware Super arrangement) columns to allow a like-for-like advised comparison.

GST may apply to advice fees.

The pattern is clear. Among advised solutions, our direct-ETF approach costs materially less than managed funds on institutional platforms — not because our advice is cheap, but because the investment engine (ETFs at 0.15%) is a fraction of the cost of managed funds (around 0.85%). You can read more about why we build portfolios this way on our investment philosophy page. Please note this approach using direct exchange traded funds is ideally suited to clients with $750,000+ per person/entity to invest.

But cheapest is not the same as best

Aware’s MySuper option is the lowest-cost line in the table, and for some people a low-cost default fund is exactly the right answer. The purpose of a fee comparison is not to crown the cheapest option — it is to make sure you know what you are paying, and what you are getting for it. Russell Investments’ 2026 Value of an Advisor Study frames advice value across four areas: asset allocation, behavioural coaching, customised planning and tax-smart investing.

In Russell’s framework, the single biggest driver of value is behavioural coaching — keeping you invested through the frightening moments when the instinct is to sell. That discipline is worth far more than a few basis points of fee, and it is exactly the kind of value a one-size-fits-most default fund cannot provide.

In Russell Investments' framework, the single biggest driver of advisor value is behavioural coaching — keeping you invested through the frightening moments when the instinct is to sell. That discipline alone is estimated to be worth 2.30% per year — far more than the cost of advice itself, and exactly the kind of value a one-size-fits-most default fund cannot provide.

The numbers behind that figure are sobering. During the 2020 pandemic selloff, investors collectively withdrew $330 billion from markets — only to miss a subsequent 12-month recovery of 63%. The same pattern repeated during the 2008 credit crisis and the 2022 inflation shock. In each case, the investors who fled locked in their losses and missed the rebound. Over the 15 years to December 2025, this "buy high, sell low" behaviour cost the average retail investor 2.30% per year in foregone returns — the difference between the S&P 500's annualised return of 14.06% and what investors actually received: 11.76%

But behaviour is only part of the story. Russell estimates the total annual value of working with a financial advisor at 4.92%, spanning smarter asset allocation (0.26%), personalised family wealth planning that goes well beyond what any robo-advisor offers (1.13%), and tax-smart investing strategies that can dramatically reduce the annual drag taxes place on a portfolio (1.23%). Taken together, the case is clear: in an age where information is freely available to anyone with a smartphone, an advisor's true value lies not in access to data — but in the judgment, discipline, and personalised guidance they apply on your behalf.

The bottom line

A reasonable advice fee in Australia is broadly 1%–1.5% p.a. plus GST — but treat that as the start of the conversation, not the end. Ask what the investments themselves cost, ask how your money is actually managed, and add the two figures together. When you do, a lower-cost investment engine can leave you materially better off over time, even after paying for quality, personal advice.

Why not take the next step and talk to a qualified and highly experienced financial planner today? LifeTime Financial Group are specialist (holding appropriate accreditations) financial planners who are ideally positioned to work with you in planning and managing your financial planning needs.

If you would like to discuss your current position or wider financial planning needs, why not call us today on 03 9596-7733? There is no cost or obligation for our initial conversation/meeting.

LifeTime Financial Group. A leading privately owned Melbourne-based Financial Planning practice with no ties to any financial institution.

This article provides general information only and does not take your personal objectives, financial situation, or needs into account. It is not personal financial advice. Tax rates, caps, and rules are current as at the 2025–26 financial year and may change. You should seek advice tailored to your own circumstances before acting.

Sources & references

• Russell Investments — 2026 Value of an Advisor Study (13th Edition). russellinvestments.com. Download your copy here

• Aware Super — Fees and costs: aware.com.au/member/what-we-offer/fees-and-costs (MySuper Lifecycle Grow / High Growth investment fees and administration fees).

• MLC — MasterKey Super & Pension Fundamentals fees and disclosure updates: mlc.com.au/personal/superannuation/fees-education

• AMP — MyNorth / North platform fees: northonline.com.au/adviser/products/fees

• ASIC Moneysmart — Financial advice costs: moneysmart.gov.au

• LifeTime Financial Group — Our Investment Philosophy: yourlifetime.com.au/our-investment-philosophy